Starting something is exciting. There are so many new things, different things to appreciate and consider, and the learning curve is rewarding enough that you feel like you are progressing nicely.

Then, hitting your end goal or target is exciting. There’s a rush of satisfaction, a sense of completion, and a chance to look back at how far you’ve come. You see the effort paying off, the small wins adding up, the pieces falling into place. It feels earned.

But everything in between? That’s the boring middle.

And that’s where most investors fail – not because they picked the wrong stock or fund, but more often than not, simply because they got bored, distracted, or scared before the real growth had time to happen.

They end up wanting to fiddle around with their investments, tinkering about and end up doing

Investing is about staying consistent in the boring middle. And that’s where wealth is built.

And in this video, I will explain how I personally handle the boring middle, which simple global fund I chose for it and how it all fits in together with my strategy.

In order to organise my investment portfolio strategy I created the Metronome portfolio

Now it’s a fairly complex concept and I made another write up on this portfolio set up that’s worth checking out for a full explanation in the link above.

The Middle of the Metronome Portfolio works in the background. It’s a place for your capital to grow passively and automatically once your dividend Base (covering your Minimum Viable Lifestyle) is established.

This layer is built around a chosen accumulating ETF broad, globally diversified funds that automatically reinvest any dividends.

That means no need for tracking payout dates, no need for decisions about reinvestment, and no need for monitoring company news. You simply buy, hold, and forget.

It’s designed for moments in life when:

- You’re earning well and want to invest surplus cash without the stress.

- You’ve maxed out your Base or tax-advantaged accounts.

- You want to build wealth for the long term (like retirement) without needing to watch the market.

Think of it as a “no-mind” portion of your portfolio: you’re not trying to beat the market, find the perfect stock, or respond to headlines. With the Middle, your job is simple—just invest regularly and leave it alone. The market, time and compounding do the rest.

And it’s flexible too: if your life changes and your income needs rise, you can reallocate funds from the Middle to the Base to increase your dividend income. It’s your overflow tank, your retirement reservoir, and your mental bandwidth protector—all in one.

In short: the Middle exists so your money can keep working, even when your main focus and attention is elsewhere. That’s the real power of no-mind investing.

In order to truly hit that no-mind status you need a reliable ETF.

If you’re completely new to this, don’t worry. An ETF, or Exchange Traded Fund, is just a basket of investments, usually stocks, that you can buy or sell like a single share on a stock exchange.

Let’s break it down without the financial jargon.

ETF stands for Exchange-Traded Fund. At its simplest, an ETF is like a basket of investments—usually made up of stocks, but sometimes bonds or other assets too. You buy shares of this basket just like you’d buy a regular stock on a stock exchange.

But here’s the major point: instead of owning just one company (like buying a share of Tesla or Tesco), when you buy one share of an ETF, you’re getting tiny pieces of hundreds or even thousands of companies, all bundled into that one fund.

That gives you an instant form diversification. If one company in the ETF does poorly, the others can help balance it out. This is a big part of why ETFs are so popular with long-term, hands-off investors, they’re built to spread risk while still capturing growth.

Now, most ETFs don’t try to beat the market. They simply track it. For example:

An S&P 500 ETF holds shares in the 500 biggest companies in the U.S.

A Global ETF might hold companies from dozens of countries, including both developed economies (like the U.S., UK, Japan) and emerging ones (like India or Brazil).

There are ETFs for specific sectors (tech, energy), regions (Europe, Asia), or strategies (dividends, ESG, etc.).

In my case, for the Middle of the Metronome Portfolio, I specifically choose an accumulating global ETF. Why?

Because:

It automatically reinvests dividends back into the fund, so there’s nothing for me to do.

It covers developed and emerging markets—so I’m not betting on one country or region.

It’s passive, so fees are low.

It works completely in the background while I focus on the other parts of the metronome and let compounding do the work.

ETFs are traded on regular stock exchanges, which means they’re liquid (you can buy or sell easily), transparent (you can see exactly what’s in them), and easy to access through platforms like Trading 212 or others.

So to sum up: ETFs let you own a lot of the market, with very little effort. They’re simple, efficient, and ideal for the long-term, no-mind strategy I use for the “boring middle” of my portfolio.

Here are the criteria I think are important for choosing such an ETF:

- Global diversification (developed and emerging markets)

- Low Total Expense Ratio (what’s known as TER)

- Accumulating dividend policy (Acc)

- Physical replication (not synthetic)

- Large fund size and high liquidity

- Tax efficiency where possible

- Trades in GBP to avoid FX transaction fees

Meeting all these criteria results in a globally diversified, low-maintenance investment vehicle designed for long-term growth. It compounds returns in the background, requiring no active management or rebalancing, while offering broad market exposure and simplicity. It’s ideal for investors who want peace of mind and steady progress without constant oversight.

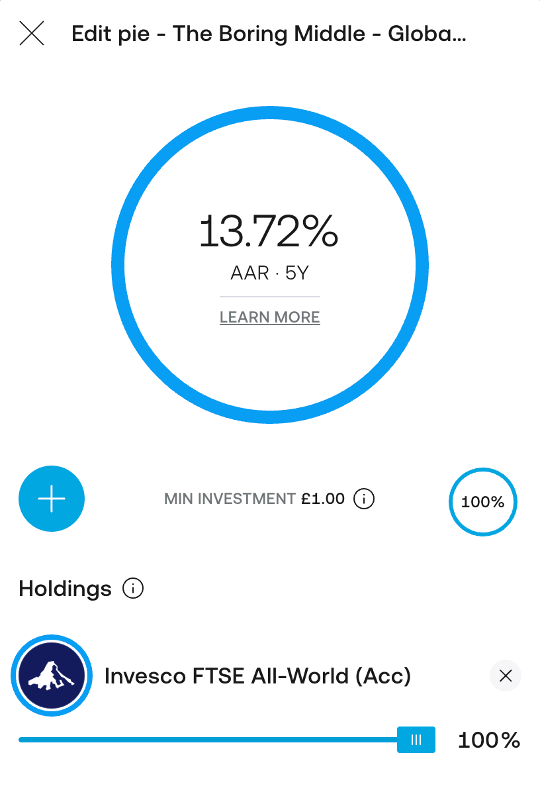

For me the ETF or fund I chose for this, that I believe satisfactorily fits the criteria, is the Invesco FTSE All-World UCITS ETF Accumulating version with the ticker symbol (FWRG).

And for convenience, as that name is a bit of a mouthful and might be difficult to search and I know that there would be questions about it… I made a pie with this fund inside it as the only component. This means that you can find it much easier on Trading 212 if you are following my public profile on there.

You don’t need to copy it or even hold it in a pie really; I just made it so that its easier for you to find. As it’s an accumulating ETF there is not even the benefit of having dividends reinvested within the pie so copying it is fairly redundant but welcome to if you prefer for whatever reason.

I will link to the pie with the ETF directly here.

And speaking of Trading 212,

If this is the first time you are coming across this pie then the chances are you are new to Trading 212, and in that case you don’t want to miss out on the sign-up offer for new users if you haven’t got it already.

**If you are new to Trading212 and looking for a promo code to get free shares please check here! You can still get a free share if your account is under 10 days old – Don’t miss out!**

Trading 212 Promo Code for The Dividend Experiment

I would also like to say that I will explain why I chose this ETF in the rest of this post but want to make the point that it’s not a recommendation or advice for you, personally. You might agree with my thoughts, or you might want to alter them slightly once you see my reasoning.

Let’s take a look…

1. Geographical Coverage

Why It Matters

Diversification is a fundamental principle of investing, helping to reduce risk by spreading exposure across different regions. A true global ETF should cover both developed and emerging markets to capture broad economic growth while mitigating localized downturns.

Comparison of Global Indexes

| Index | Developed Markets | Emerging Markets | Number of Countries |

| MSCI World | Yes | No | 23 |

| MSCI ACWI | Yes | Yes | 49 |

| FTSE All-World | Yes | Yes | 48 |

The FTSE All-World Index, in this case tracked by FWRG, includes a wide range of large and mid-cap stocks from approximately 50 countries. This means investors gain exposure to high-growth markets like China, India, and Brazil, which might be excluded in other ETFs focusing solely on developed economies.

Emerging markets often experience higher growth rates than developed ones. By investing in FWRG, you tap into future growth drivers, ensuring your retirement investments benefit from global economic expansion.

A Balanced Approach is Best

Now you might be thinking, if Emerging markets are higher growth so why bother with the rest of the global fund?

Rather than going all-in on emerging markets, I believe a global ETF like FWRG offers the best of both worlds (excuse the pun):

- Exposure to emerging market growth (India, China, Brazil)

- Stability from developed markets (U.S., Europe, Japan)

- Lower volatility and better risk-adjusted returns over time

Going all-in on emerging markets might seem appealing due to their historically higher growth rates, but I think a balanced global approach is more sensible for long-term investing.

Emerging markets tend to be more volatile, prone to political instability, currency fluctuations, and weaker financial oversight. During downturns, they often fall harder and take longer to recover. For instance, the MSCI Emerging Markets Index dropped over 50% in the 2008 financial crisis, compared to a 40% decline in the MSCI World Index, and some countries, like Brazil and Russia, took more than a decade to recover.

Another problem with going all in on emerging markets is that they often face challenges like higher inflation, liquidity constraints, and restricted capital movement in some regions.

Developed economies like the U.S. and Europe still lead in innovation, corporate governance, and economic stability. The S&P 500 alone accounts for about 40% of global equity markets, reinforcing its influence. So, by investing in a balanced global ETF, investors can capture emerging market growth while minimising excessive risks, aiming for long-term stability.

2. Total Expense Ratio (TER)

What is TER?

TER represents the annual percentage cost of managing the ETF. It includes administrative fees, management costs, and operational expenses, reducing your net returns over time.

ETF Cost Comparison

| ETF | TER (%) |

| Vanguard FTSE All-World (VWRL) | 0.22 |

| iShares MSCI ACWI (SSAC) | 0.20 |

| Invesco FTSE All-World (FWRG) | 0.15 |

With a TER of 0.15%, FWRG is one of the more affordable global ETFs, though the SPDR MSCI ACWI ETF (Ticker: ACWI) offers an even lower TER of 0.12%.

It actually lowered its fees after I had already chosen FWRG and I decided to stick with FWRG rather than hopping between any fund that decides to lower its fees at any given time.

However, FWRG still remains a strong contender due to its accumulating structure and broad market exposure, making it a cost-effective choice for long-term investors.

Up to you if you think that is reasonable justification or you think I am just being lazy here and not switching to the lowest fees!

The Compounding Effect of Low Fees

Assuming a £50,000 investment over 20 years with an 8% annual return, here’s how TER impacts final portfolio value:

| TER | Final Portfolio Value (20 Years) |

| 0.15% | £233,047 |

| 0.22% | £227,918 |

| 0.30% | £222,580 |

Assuming all else remains equal – lower costs increase your retirement savings, making FWRG a solid option here.

3. Dividend Policy – Accumulating vs. Distributing

Understanding Dividend Policies

ETFs can either:

- Distribute dividends (payouts in cash to investors) these will have (Dist) at the end of the name

- Accumulate dividends (reinvest them within the fund) these will have (Acc) at eh end of the name

Invesco FTSE All-World UCITS ETF Acc (FWRG) has “Acc” in the name so FWRG is an accumulating ETF, meaning dividends are automatically reinvested, increasing the share price and maximizing long-term growth.

Why Accumulation Works Best for what I need

- No manual reinvestment required, so more aligned with the “no-mind” approach I mentioned earlier

- Dividends compound over time by themselves

- More efficient for tax-free accounts like SIPPs etc. (which, incidentally, is where I am holding it in the most part)

If you are holding outside a tax-advantaged account then it’s a bit more complicated, but I can’t talk about that without a tonne of different disclaimers so we will save that for another video!

4. Replication Method – Physical vs. Synthetic

This one is a little abstract but still worth mentioning, if you zone out of this short section I can completely understand.

How ETFs Replicate an Index

- Physical Replication: The ETF directly holds the underlying stocks

- Synthetic Replication: The ETF uses derivatives to mimic index performance

FWRG follows a sampling-based physical replication method, meaning it holds a representative selection of stocks rather than every single company in the FTSE All-World index.

So What?

Physical ETFs have greater transparency and lower counterparty risk whereas Synthetic ETFs carry risks related to derivative contracts.

For what I am looking for physical replication is generally preferable due to its reliability and lower risk profile. No need to increase obscure risks for relatively little benefit.

5. Fund Size & Liquidity

A larger fund typically has:

- Lower bid-offer spreads

- Greater liquidity (easier to buy/sell shares)

- Higher investor confidence

FWRG has an AUM of approximately £764 million, which provides reasonable liquidity and stability, though larger ETFs may offer even narrower bid-offer spreads. I think the largest is likely to be VWRL by Vanguard but, to be honest, I think this would ultimately be a probably pretty negligible difference though happy to be corrected in the comments if you have evidence to the contrary!

6. Domicile & Tax Efficiency

Why Domicile Matters

The country where an ETF is domiciled affects taxation, particularly withholding tax on dividends from U.S. stocks. A tax-efficient domicile ensures that investors retain more of their returns.

Comparing Ireland vs. Luxembourg for ETF Domicile

- Ireland-Domiciled ETFs benefit from a 15% U.S. withholding tax rate due to the U.S.-Ireland tax treaty. This ultimately means investors keep a larger portion of dividends from U.S. stocks.

- Luxembourg-Domiciled ETFs however are typically subject to a 30% U.S. withholding tax, as Luxembourg lacks a favourable tax treaty with the U.S. Some Luxembourg ETFs use more complicated tax-efficient structures, but Ireland remains the preferred domicile for tax efficiency.

Why This Matters for FWRG

FWRG is domiciled in Ireland, meaning it benefits from the lower 15% U.S. withholding tax, making it more tax-efficient for holding U.S. stocks within a global portfolio. Over time, these tax savings can significantly improve net returns, especially for long-term investors.

7. Currency Exposure

FWRG trades in GBP, eliminating foreign exchange (FX) fees when buying through UK platforms.

That being said, underlying assets are priced in multiple currencies, so currency fluctuations will still affect performance. Even though you buy and sell the ETF in GBP, its underlying holdings are in various global currencies such as USD, EUR, and JPY. This means that if the GBP strengthens against these currencies, the value of those foreign holdings decreases when converted back to GBP, reducing the ETF’s performance.

Similarly, if the GBP weakens, the value of foreign holdings increases, boosting returns. So you should be aware that while trading in GBP avoids direct FX transaction costs on platform, currency movements still play a role in long-term returns.

Why FWRG is the Best Global ETF for me

With broad global exposure, low costs, tax efficiency, and a structure optimized for long-term growth, FWRG is my top choice for a ETF. While other ETFs may have slightly lower fees, FWRG offers an excellent balance of cost, diversification, and efficiency, making it an ideal investment for long-term retirement savings.

Going straight to the lowest costs (TER) as a strict rule means that you will be always having to keep up to date with the current fee structures which takes away from the intention of it being “no-mind” at least in my opinion.

I am happy with FWRG as the choice for the “middle of the metronome” section of my portfolio and don’t feel the need to change it. But there is one more inevitable question I will no doubt get that I should address.

Why I Choose Global Over Just the S&P 500

If you’ve spent any time on finance forums, you’ve probably seen the go-to advice: “Just invest in the S&P 500, bro.” It’s repeated so often that it’s basically a meme at this point. People treat it like gospel—even when they don’t really understand what it is or what it exposes them to. And to be fair, it’s not terrible advice. It’s simple, accessible, historically strong, and backed by some of the biggest, most powerful companies in the world.

But that simplicity hides a few things. The S&P 500 is still just a list of 500 large U.S. companies. That’s it. It doesn’t include smaller-cap stocks. It doesn’t include emerging markets. It doesn’t include the other 95% of the world’s population or economic activity. And while those companies are global in revenue, you’re still investing only in one country’s stock market, one currency, and one political system.

That might be fine when the U.S. is booming, but what if that changes? Recency bias makes the S&P 500 look like the only smart option—but if you zoom out a few decades, there have been plenty of periods where international stocks outperformed U.S. ones. If you’d been investing in 2013 and looked back 10 years, U.S. stocks were underperforming international markets more often than not.

A global fund—like an all-world ETF—spreads your bets across developed and emerging economies, thousands of companies, multiple currencies, and a wider range of sectors. It captures growth wherever it happens. And while the S&P might do better during bull markets, a global fund offers better balance during downturns. It’s not about performance alone—it’s about resilience.

So why do I go global? Because I don’t want to guess which country wins next. I want to own the whole race.

Final Thoughts

At the end of the day, the Middle of the Metronome Portfolio isn’t supposed to be flashy. It’s not where the excitement happens. It’s where the compounding, the consistency, and the hands off wealth building take place. Without needing your constant attention or emotional energy.

By choosing a globally diversified, low-cost, accumulating ETF like FWRG, I’ve created a part of my portfolio that keeps ticking in the background, no matter what’s going on in the markets, or in my life.

It’s not about picking the perfect stock or reacting to headlines. It’s about staying invested, staying calm, and giving your strategy the time it needs to work.

The boring middle might not get much hype online, but it’s where most of the real progress happens.

So if you’re building a portfolio for the long haul, one that supports your freedom, your peace of mind, and your future – The Boring Middle is exactly where you want to be.