On how to overcome investing FOMO by building a disciplined, goal-focused portfolio that keeps emotions and hype in check.

Your friend just showed you how much they made by investing in some random “Dogecoin crypto” something.

You saw a Reddit post about someone buying an apartment with the proceeds of their investment in lean hog futures.

Your dad just messaged you about a startup drone company that’s been taking off lately,

And no,

It’s not one of his usual puns.

This doesn’t feel good.

In fact, it can actually be quite dangerous and cause you to stray from your path of sustainable wealth building into all sorts of different fields of investments that you simply have no clue about.

This is FOMO, the Fear Of Missing Out.

What is FOMO?

FOMO, or fear of missing out, is when investors feel anxious about not joining others in profiting from a particular asset, leading to impulsive and often poor investment decisions.

Acting on FOMO means skipping research, which can result in overlooking risks and making uninformed choices.

This behaviour can lead to buying assets at their highest prices and selling when prices drop, which goes against the basic investment principle of buying low and selling high.

Emotional decision-making driven by FOMO can cause stress and lead to seeking only information that confirms one’s decisions, ignoring important facts that show you might be wrong.

Following the crowd, or herd mentality, often leads to overcrowded investments, reducing profit potential and possibly creating market bubbles where asset prices are way above their true value.

When these bubbles burst, sharp losses can occur.

Focusing on hot trending assets can cause investors to miss out on better opportunities and neglect diversification, putting too much money into one asset or sector.

Obviously, suffering from this FOMO isn’t great for long-term wealth building; in the worst cases, it can even lead investors to stop investing completely.

How to Avoid Investing FOMO

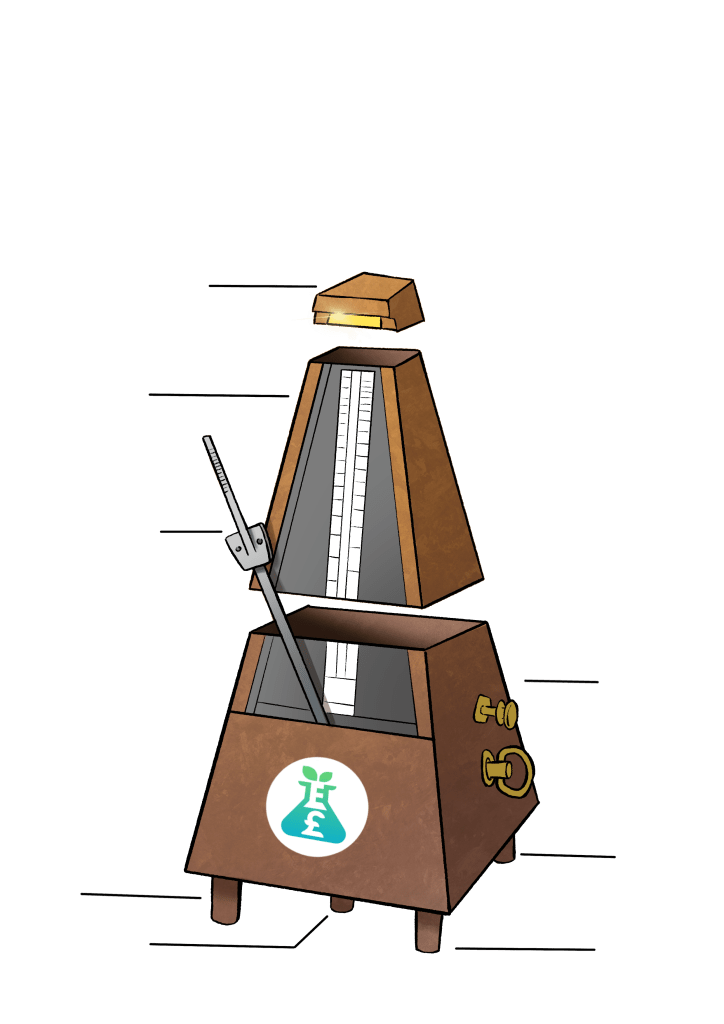

This metronome is a representation of how I organise my portfolio.

It works like this:

- Four legs: these are the four important things you need to have before you even start investing.

- The base and ticker: this is the income that fuels the rest of your investment and potentially your lifestyle later on.

- The middle: this is the set-and-forget part of your portfolio.

- The tip: these are the risky bets, and they should only be about 3–5% of your entire portfolio at max.

What does all this have to do with FOMO?

Well, each stage has some link on how to avoid it.

Let’s go through each stage and how they help in avoiding the fear of missing out.

The Four Legs

The four legs that support the metronome portfolio are:

- Income

- Emergency fund

- Knowledge

- Emotional balance.

Income

Income is necessary, as it’s the main flow into the portfolio.

It doesn’t have much impact on FOMO, though.

Most people who suffer from investing FOMO will have an income, and that’s part of the problem.

Emergency fund

An emergency fund is very important for investing, as it provides a safety net so you don’t need to interrupt the compounding of your investments.

Again, however, it’s not really applicable to investing FOMO avoidance much at all.

Knowledge

Knowledge, on the other hand, is key. It’s important to know that, in general, the people who make money from these fast-rising investments are few and far between.

By the time you’ve heard about it, it’s probably too late anyway.

Often, the ones that do benefit end up holding on too long and ride the fall back down too.

This happens more than you’d expect, especially with big stories like cryptocurrency.

If you only see people bragging about the gains but never mentioning their losses, you’ll naturally think that everyone is winning except for you.

Naturally, people only want to share their positive investments, as it protects their ego.

This leaves a situation where people are only sharing the fast money-making plays, and you’re comparing them to your own situation.

Just like on Instagram, people are sharing their life’s highlight reel, and the first step to combat that is knowing that this is the case.

And if you want to go deeper on this — how to invest properly and how the Metronome Portfolio works — the best place to do that is The Dividend Academy.

Emotional balance

This final leg lines up nicely with knowledge.

Emotional balance means you need to be mentally prepared for your portfolio to experience a 50%+ downturn at some point.

It means you have a plan and you’re content with the outcome of it.

It’s quite simple, but not easy at all – it goes against the psychological traits humans have evolved with.

The Base

This is where The Dividend Experiment comes into play.

This is the income-investing side of the portfolio, and the goal here is to first calculate the amount of money you’d need to live a Minimum Viable Lifestyle.

Once you have the Minimum Viable Lifestyle target amount, then you work towards building a portfolio that pays your bills.

How does the base help with Investing FOMO?

Working on this in and by itself is incredibly rewarding, and it hits similar dopamine levels as chasing gains.

In fact, it’s much better, as the results are a stepped increase in income every time you add more to the portfolio; the 1p dividends become 10p, the 10p become £1, the £1 become £10, etc.

This is possibly why dividend investing is so popular; you can see the growth in income over time.

If you wanted to take out the money from the base of the portfolio to invest all in some biopharmaceutical electric vehicle penny stock, you’d have to reset all of your progress so far.

When you’re building a dividend portfolio, rightly or wrongly, it does feel as though you’re building something, and psychologically, that is huge.

Dividend investing isn’t a get-rich-quick kind of thing, like the FOMO-type things that are attractive, but instead, once you start building it, it becomes difficult to undo your hard work.

The Middle

The Middle is where the bulk of your investment deposit ultimately ends up.

It’s also the simplest one to deal with, as there are relatively few choices here.

You basically select an index fund ETF-type investment that covers a broad range of stocks, possibly even across multiple stock markets.

My personal preference at the time is Invesco FTSE All-World UCITS ETF (Acc), ticker symbol FWRG.

To summarise: it’s an exchange-traded fund that tracks the FTSE All-World Index, providing diversified exposure to large and mid-cap stocks across both developed and emerging markets globally.

As an accumulating fund, it reinvests dividends, potentially enhancing long-term returns through compounding.

The ETF is UCITS-compliant, ensuring adherence to EU regulatory standards for investor protection, and offers a cost-effective, liquid option for investors seeking broad global equity exposure.

So basically, I buy this in The Middle part of the portfolio and then don’t really think about it again.

Now, you might prefer a different specific ETF or a combination of them, even, but the premise of the middle of the metronome is the same, it’s basically a set-and-forget portfolio that you put excess investments into.

Avoiding Investing FOMO in the Middle

It’s a bit tricky, but it comes down to this: only a very small number of actively managed funds can beat the stock market over the long term.

These have a large amount of resources, information, and even staff working on doing exactly this: you don’t.

It’s going to be much harder for people like us to beat the market.

So, if we can’t beat it, why not join it?

This kind of goes to the concept of “no mind” that’s popular in Zen Buddhism and Eastern philosophy, where, if you want to seek peace, then it’s better to have no mind.

This kind of investing is about as close to “peace” as you can get.

The Tip

This part is the allocation of the portfolio, where you can take on the risk, which serves as a contrast to the other sections.

It acknowledges the human nature of wanting to take higher risks for potentially higher rewards.

This section includes high-risk, high-reward type plays that may tempt you, such as hyper-growth stocks, penny stocks, moonshot-type plays, and even cryptocurrencies.

However, it’s important to keep the tip to a minimum percentage of your overall portfolio.

It’s recommended that the tip section should not exceed 5% of your total portfolio, preferably less than 3%.

If you prefer to skip this section entirely, that’s entirely up to you and can be a wise decision.

However, many individuals enjoy taking bigger risks or exploring moonshot opportunities with significant potential rewards.

The key is to manage these risks in a way that won’t jeopardise your entire portfolio or hinder your overall progress.

How Does the Tip Avoid Investing FOMO?

It leans into the same primitive, ape-like urge that humans have, to take risks and get bigger and better rewards, but in a controlled and organised way.

It won’t make you a crypto billionaire if you only allocate 3 to 5% of your portfolio to some next altcoin the guys down the street are talking about, but it won’t flatten you either if it goes wrong.

And let’s be honest, the odds are probably ultimately not in your favour anyway.

This doesn’t mean you have to invest a little chunk of your portfolio into something stupidly high-risk just for the sake of it.

Does It Work?

Only time will tell for something like this, but so far, so good.

A big challenge would have been seeing people make huge amounts of money on stocks like Nvidia recently, which is up 122% year to date.

Now, Nvidia is a company I thought was well-run and is in an industry that is likely to be in demand.

It’s reasonable that I could have invested in it and missed out, but here’s the thing:

It didn’t fit my plan to invest in it as an individual stock.

And it’s a component of the ETF in the middle that I talked about earlier, so I don’t feel the need to beat myself up or join in on the hype.

In fact, I don’t feel much of anything about it at all.

You can’t lose money on stocks you don’t own, and it’s better to stick with a well-thought-out plan that suits your own goals.