On the common investing mistakes beginners make and how to avoid them to build smarter, long-term wealth.

Over the past 20 years, the average investor’s annual return has been only 3.6%.

This means that buying a house and living in it is actually a better investment than the average investor.

But that doesn’t mean that you have to be average.

This article takes you through the common mistakes that a beginner investor will probably make while taking the first step in investing.

This way, you will have the idea of how to fix or how to avoid those mistakes and perform better than the average investor.

Here is the list of some common mistakes in investing.

Lack of Research

Pets.com was an online store that sold pet supplies.

It started in 1998 and went public in February 2000 during the dot-com bubble, when many internet companies were getting a lot of attention.

Many investors bought Pets.com stock because of the hype around internet businesses.

They didn’t really understand how the company made money or the challenges they faced.

Pets.com had a business model that didn’t make sense because they were selling products at a loss.

By the end of 2000, just 9 months after its IPO, the company ran out of money and announced it was shutting down.

The stock price dropped from $1 per share to almost nothing.

This showed how risky it can be to invest in companies based on hype without understanding the business, leading to big losses for many investors.

Many of the new investors lose their hard-earned money or lose mostly all of their capital by diving into an investment without proper research.

It’s the first mistake that a beginner often makes, mainly because they’re misinformed or eagerly want to make quick cash.

In today’s world, doing thorough research is very easy.

With the internet, you can quickly find all the information you need with just a few clicks, and this includes details about companies, market conditions, expert analysis, and much more.

Whether you’re checking on a company’s health, its recent performance, or the current state of the market, everything is readily available online.

This helps you make smarter decisions before investing your money, ensuring you understand all the important details beforehand.

Ignoring Fees

Fees and expenses associated with investments will eat into your returns over time if not managed properly.

Every transaction you make will have some small fee, and sometimes, in other platforms, they incur hidden fees too.

These expenses might seem small, but they can actually add up and significantly impact your overall investment performance.

For example, say you had a £10,000 investment which you held for 30 years with a 2% fee.

The investor would receive a return of 5% and would end up with just over £24,270.

But with a fee of just 0.5% and the same return of 5%, that £10,000 fund would be worth around £37,454.

That’s a huge difference of about £13,180

Which goes to show the difference fees can make to the size of your investment.

Ideally, your investment platform and fund choice charges as low fees as possible.

The platform I recommend for most users and most use cases is Trading 212.

Lack of Diversification

Employees at the infamous Enron company lost a lot on one fateful day in December 2001.

They had been getting their salary from Enron, then investing a portion of it for their pension back into Enron.

When Enron went bankrupt, it was a financial disaster for them as they lost both their savings and income all at once.

Enron Corporation, once a major American energy company, became infamous for a massive accounting fraud scandal, leading to its bankruptcy in December 2001.

Enron stock soared to $90 a share in 2000 but collapsed to less than $1 by the end of 2001.

In contrast, the S&P 500 Index, representing the 500 largest US companies, experienced volatility during the same period due to the dot-com bubble burst but eventually recovered and continued to grow.

This comparison really highlights the total loss investors faced with Enron versus the long-term growth and stability of a diversified portfolio like the S&P 500.

This kind of disaster happens when you don’t diversify your investments.

Putting all your money into one type of investment is very risky.

Many beginners make the mistake of investing only in what’s currently popular or has done well recently, but this can lead to major losses if the market changes.

To avoid this, spread your investments across different areas.

For example, while investing a lot in tech stocks might seem smart when they’re booming, your whole portfolio could suffer if the tech market crashes.

Instead, also invest in other areas like healthcare, consumer goods, and things like bonds.

This way, if one sector performs poorly, the others can help balance things out.

Diversifying helps you manage risk better and increases your chances of getting good returns over time.

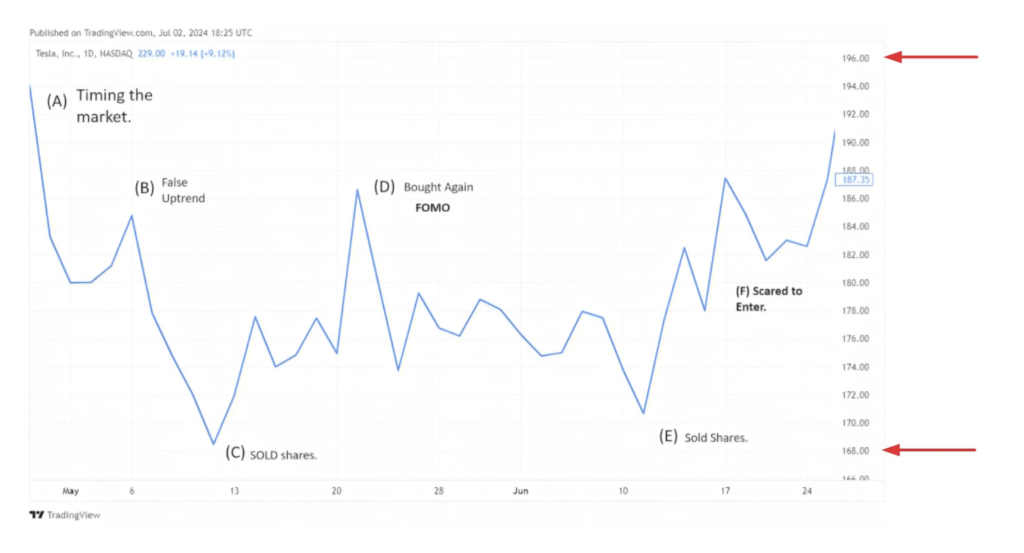

Timing the Market

Let’s examine what happened recently with Tesla to illustrate a common investing mistake.

As depicted in the chart from TradingView, Tesla’s stock price has shown significant volatility, initially dropping from $196 to $168 rapidly.

It then fluctuated before rebounding to $197.

This example vividly highlights the pitfalls of trying to time the market.

Consider John’s scenario: hearing speculation that Tesla might decline at Point A, John attempted to time the market.

He planned to enter a position upon signs of recovery.

When a slight recovery appeared at Point B, John invested $11,000, confident in his timing.

However, the stock soon showed a false uptrend and dropped again to Point C.

Disappointed, John sold his shares, hoping for a better opportunity.

John waited for the stock to stabilise and show clear signs of recovery.

When the price finally rose above his previous entry point at Point D, he entered the market, this time with greater determination to time it perfectly.

But yet again, at Point E, John sold prematurely, driven by emotional fears of another downturn.

Ultimately, John missed out on potential gains and lost his initial capital.

The stock continued its upward trend all the way to Point F, illustrating the difficulty of predicting market movements accurately and the risks associated with emotional decision-making in investing.

Many beginners make the mistake of trying to predict short-term market fluctuations.

They buy when prices are high due to hype or sell during downturns out of fear.

Attempting to time the market and making emotional decisions is the hallmark of poor investing.

Successful investors, on the other hand, stay disciplined and focus on long-term goals, ignoring temporary market movements.

Emotional Investing

One well-known example of emotional investing involves GameStop, or GME stock.

In early 2021, GameStop became the centre of a speculative frenzy driven by individual retail investors on forums like Reddit WallStreetBets.

The stock price skyrocketed from around $18 in early January to over $480 by the end of the month.

This massive increase was fueled by social media hype and a short squeeze initiated by retail investors targeting institutional short sellers.

Many retail investors bought GameStop shares not based on traditional financial analysis but rather on the belief that the stock would continue to rise rapidly due to momentum and community sentiment.

This surge in price was driven largely by emotions such as excitement, fear of missing out (FOMO), and a desire to defy Wall Street expectations.

However, as the initial hype subsided, the stock price experienced significant volatility and eventually declined sharply.

This scenario illustrates how emotional factors can drive investors to make decisions that are not necessarily grounded in fundamental analysis or long-term strategy, leading to significant financial risks.

Emotional investing can result in substantial gains for some, but it often comes with high volatility and potential losses when sentiment shifts or reality sets in.

This happens because emotions like fear can cloud our judgment.

For example, when the market goes down, fear of losing money can cause people to sell their investments hastily.

This impulsive reaction is not part of a well-planned investment strategy and can mean missing out on potential long-term gains when the market recovers.

To avoid these risks, it’s important for investors to stay disciplined and plan strategically.

Stick to a carefully thought-out investment plan that matches your long-term goals and how much risk you can handle.

Ignoring Risk Tolerance

In 2018, Facebook’s stock experienced a sharp decline due to data privacy concerns and regulatory scrutiny.

Many investors panicked and sold, but those who aligned their investments with their risk tolerance and held on to their shares saw recovery as Facebook addressed the issues and regained market confidence over time.

This highlights the importance of staying true to your risk tolerance and long-term investing strategy during market turbulence.

This occurs because risk tolerance isn’t just a theoretical concept; it profoundly influences how investors behave.

When individuals ignore their risk tolerance, they may struggle to cope with the ups and downs of their investments.

This mismatch can lead to hasty decisions, like selling investments in a panic or exiting the market prematurely, which can significantly undermine their long-term financial goals.

To avoid these pitfalls, investors should prioritise understanding and sticking to their risk tolerance levels.

- Start by evaluating your financial goals, time horizon, and how comfortable you are with market fluctuations.

- Determine what kind of investor you are, aggressive, moderate, or conservative, and that way you’ll know when to give up and when to wait.

Not Having a Plan

Investing without a clear financial plan is like travelling without a map; it’s risky and often leads to bad decisions and missed chances.

Statistics show that many investors who don’t have a structured plan end up with lower returns and unmet financial goals.

This usually happens because people forget to think long-term.

Without clear goals, a timeline, and an understanding of how much risk you can handle, you might make impulsive decisions based on short-term market changes or emotions.

This shortsighted approach can slow down your wealth growth and delay reaching financial stability.

To avoid these problems, it’s important to create a solid investment plan from the start.

Begin by setting specific goals and timelines that match your financial dreams and comfort with risk.

A good plan acts as a guide, helping you make smart investment choices that lead to steady growth and stability.

Regularly review and adjust your plan to stay on track with your long-term financial goals as your situation and the market change.

Conclusion

Overall, knowing these common investing mistakes ahead of time gives you a real edge.

You’ll be able to avoid the same traps that many investors fall into.

By staying clear of these errors, you can improve your investment strategy and have a better shot at reaching your financial goals.

Understanding these mistakes helps you protect your money and can lead to better returns over time.

Plus, staying disciplined and continually learning about the market will help you make smarter decisions.