**If you are new to Trading212 and looking for a promo code to get free shares please check here! You can still get a free share if your account is under 10 days old – Dont miss out!**

Trading 212 Promo Code for The Dividend Experiment

Hi, you have probably just come across this pie – The UK income factory – on Trading 212.

Now you might like the sound of it, but there are some things you should know and be aware of before you jump in.

So I highly recommend you have a watch of this video to have a better idea of what it is, how it all works and how to maintain your copy in the future.

What we will cover

- Brief description of why I made this pie

- What it is

- What it is not

- How pies work (generally)

- Minimum recommended requirements to get started

- How long it takes until dividends come in

- How to view dividend yield

- The stock categories

- Why I chose the stocks

- How to get updates if it changes.

- How to discuss more about this pie

if you are new, I really suggest you read through all of it. Even on the topics you think you are confident with there is likely nuance you haven’t considered. But before we get started… if this is the first time you are coming across this pie then the chances are you are new to Trading 212, and in that case you don’t want to miss out on the sign up offer for new users if you haven’t got it already.

Introduction

This pie came about as I had already made the Almost Daily dividends pie and there were many requests for a dividend pie that was based solely on UK stocks.

The idea behind it was that US stocks charge a 30% withholding tax, which is then reduced to 15% when you sign a W8 Ben form in the UK (but your own tax jurisdiction may vary) and this takes a chunk out of dividends.

Then as you invest in USD when your currency is something other than USD you are subject to exchange rate risk.

There was a demand for me to make an income based pie that was in GBP and listed on the UK stock indexes and the result was this pie.

The name Income factory came from a book by Steven Bavaria which is a good way to think about Dividend or Income investing. Not all of it applies to Non-US investors but I think I would recommend it as a way to thin about investing for income versus for growth.

Now before we get into the details of the pie I would just like to address…

What this pie is NOT

Need to address this first of all as they are common misconceptions but:

This pie is not a true set and forget portfolio. You are copying a template. Its not a live copy that updates and changes as soon as I make any buys or sells.

It’s like you get some instructions of how to organise a series of 50 stocks and then you invest money into that.

It’s also not the “UK version” of the almost daily dividends pie. This seems to be a common misconception but there are way fewer dividend payment dates here and the goals are not aligned in the same way.

It’s also not only for UK investors or UK accounts on Trading 212 – the UK doesn’t charge withholding tax on dividends (at the time of making this video at least!) so investors from elsewhere will benefit from the same yields.

Though please bear in mind the specific taxation of dividends in your jurisdiction

This is also not investment advice or a recommendation. I’m not endorsing every stock in the pie individually. This structure reflects my own strategy for this pie’s goals and preferences towards that at the time of creation, but it may not suit your needs, risk tolerance, or financial goals.

Now, what this pie is…

The UK stock market index or the FTSE 100 has typically had returns of 6-7% on average over the long term. Some years were higher, some lower but that’s pretty much been the average.

Now the idea of an income factory portfolio is to get most of that return through, well income. The target for this pie is to get a 5% dividend yield then capital appreciation to top up the rest of the average return. This means it is, in theory, less susceptible to the variations of the market and closer to a stable income producing portfolio that generates the returns through paying out the dividends to us.

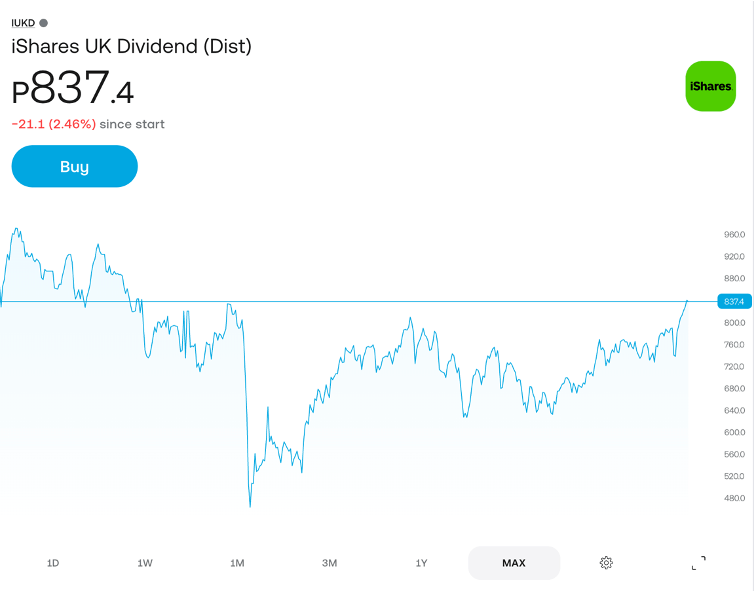

There are ETFs that do this, the one that I try to benchmarked this portfolio to is IUKD.

By benchmark I mean it’s like a rival, something we try to beat.

On the face of it, these two portfolios are roughly the same kind of thing.

IUKD’s goal is to track the performance of an index composed of 50 stocks with leading dividend yields from UK listed companies, excluding investment trusts.

Its current yield at time of writing is 5.03%

So I am targeting a yield of 5%, roughly the same then aiming for outperformance compared to IUKD with this pie.

Now the thing that has put me off investing in IUKD directly is that it charges a fee to hold, like all ETFs, but this one is relatively high for what it is.

IUKD charges a 0.4% fee per year to hold it, which I feel is higher than it could be for what it actually does – essentially screen for the highest yielding stocks in the FTSE 100 and put them into a fund.

So the goal is to see if this UK income factory can outperform it.

Then I don’t want to take excessive risks with this pie, especially as its made with a view for people who have been looking for it to copy it so I also want it to have low beta, low volatility and the stocks to have relatively high market caps – so a lot of the companies on the holdings list you will recognise as being from the FTSE 100.

Many investors will be comparing investing this pie to the return on cash.

Though I don’t necessarily believe that it is a good comparison as I explained in this video. (which is worth watching if you are not sure why they are a bad comparison by the way, not enough time in this video to explain in full detail as I imagine its going to be longer one already!)

With that in mind, I would still aim for the yield of this pie to be comfortably above the yield on uninvested cash on trading 212 at any given time.

So a higher % of income than holding cash with the potential for capital appreciation too.

That’s the aim, at least.

Recommendations

The minimum size for the initial investment is £50 and this is a reasonable starting point to get all the dividends you are entitled to without it rounding down to below one pence, however £100 would be more comfortable in case you are watching some point in the future.

For future reinvestments or additions then £50 is fine.

If you are a tax resident of the UK and you still have allowance I don’t see a reason why you would use the invest account to hold this pie over the ISA account. That pretty much goes for all investing but especially dividend investing.

If you are not sure about the difference in the account types I have made this video

explaining the difference between them.

Now of course whichever account you choose is at your own discretion; I just don’t personally see a use case for that.

Then when you invest in stocks the general guideline or thought is that you should invest with at least a 5 year holding period in mind, so any stock can fluctuate and perhaps be negative in the short term but over the long term you have a better chance of being ahead.

Past performance is not a guarantee of future returns, however.

How do dividends work?

Dividends are paid out by companies to reward their shareholders, but to receive a dividend, you must own the stock by a specific date, known as the ex-dividend date. Here’s how it works, there are 4 relevant dates:

- Declaration Date: The company announces the dividend and sets key dates, including the ex-dividend date.

- Ex-Dividend Date: This is the crucial date. To be eligible for the dividend, you need to own the stock by the day before this date. If you buy on or after the ex-dividend date, you’ll miss that particular payment.

- Record Date: This is when the company records the shareholders eligible to receive the dividend.

- Payment Date: This is when the dividend is actually paid out to shareholders.

If you invest in a dividend portfolio (like this pie) today, you’ll need to wait until future ex-dividend dates for each holding to qualify for dividends.

Dividends aren’t paid out immediately after purchase because they follow this scheduled cycle.

As each stock in the pie reaches its ex-dividend date in the coming weeks or months, you’ll gradually start receiving dividends from different holdings, eventually leading to more frequent payments as the cycle continues.

In short, while dividends don’t start immediately after investing, with time and reinvestment, you’ll build a steady stream of income as each component in your pie hits its payout schedule.

So, it’s not really a question of “How long until I get dividends?” and there being a simple timeline answer as it completely varies on when you started and which dividends you are entitled to since.

How to View Dividend Yield

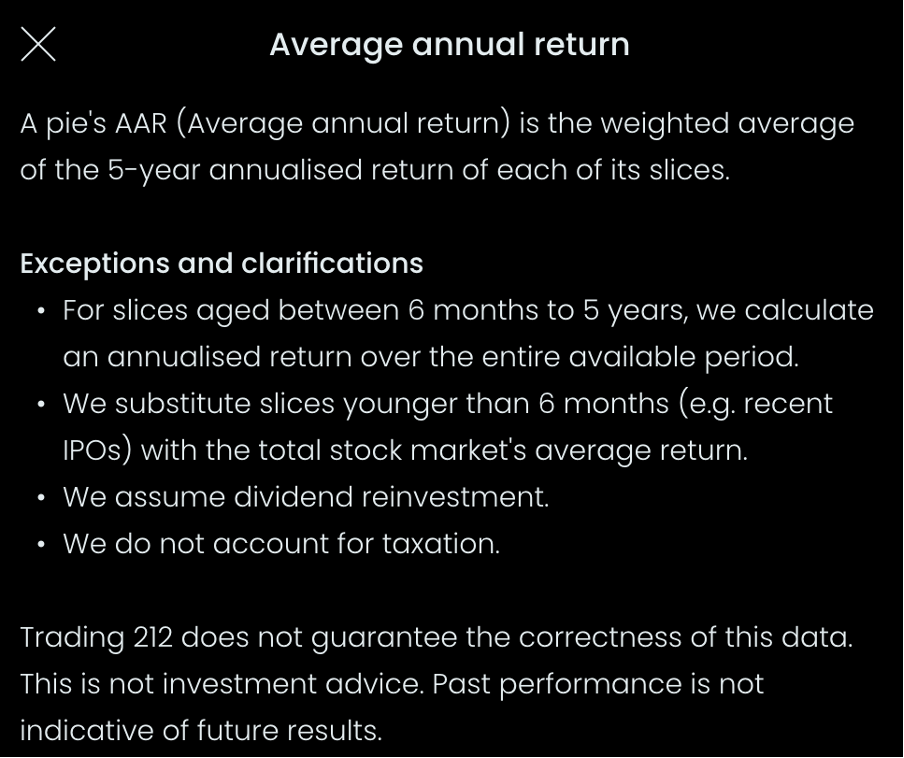

Another very common question that people ask on the pie is what is the current yield of the pie?

People often get confused between the yield and the “AAR” that it displays on the pie screen on Trading 212. For that reason, I will just quickly explain the difference and then show you how to check the yield live at any time.

Dividend Yield is like the “income” percentage you earn from a stock each year, based on its price. Think of it as how much cash you get back just from holding the stock.

So, if you invest £100 into a stock with a 5% yield then you are getting £5 back, that’s the simple view on dividend yield.

The thing is income from dividends is only one part of the story of investing in stocks, the price of the stock goes up and down too – and that’s where the AAR figure that is shown on the Trading 212 screen comes in.

AAR (Average Annual Return) shows the overall yearly growth of your investment, including both dividends and any increase in stock price. It’s the big-picture measure of how well the investment grows each year on average.

The one shown on Trading 212 is actually the average over the past 5 years.

In short,

Dividend Yield = income only,

while AAR = income + growth.

That means don’t interpret the yield as all you get from your investment, the share price changes impact your return too.

It also means don’t interpret the AAR as how much you will get paid in dividends.

I have found copiers getting these two percentages mixed up is very common so worth adding this section in here.

How to Get Updates if the Pie Changes

If your pie is linked and you have notifications on, then when I make a change to the pie you should get a notification telling you that you will need to update in order to keep to the current template of the pie.

That being said, there are a few problems with this system.

First if you edit or customise the pie yourself you become “unlinked” or “delinked” or whatever the terminology is and might not receive notifications. Secondly the notification doesn’t give any indication of why I made the change, it just asks you to accept the change or not and there is no reasoning for the change whatsoever.

So, to counter these two problems I set up an email list that I send out the email that gives a thorough explanation of what I changed and why I changed it and that will give you some background information so you can make your own decision.

That means if you want to make some edits to the pie but still want to know what’s going on with the original then join the email list.

It’s also there for people who don’t tend to check their notifications often enough but will pay attention if there is an email coming in.

It is quite sad to see comments like:

“when are you replacing this certain stock? It’s been underperforming recently”

Where I had made an update many months prior that removed that stock, to the point I didn’t even have a reason to keep track of it anymore.

So in summary – if you feel fine with copying the template and then dealing with it after that then you can rely on the notification.

However if you are serious about keeping it up to date then it’s worth joining the email for the full reasoning behind the change.

And then finally…

Stamp Duty

When investing in specifically UK-listed stocks on Trading 212, a stamp duty of 0.5% is automatically applied to each purchase. This applies equally whether you’re buying manually or through a pie. The charge is built into the transaction so it slightly reduces the amount actually invested. For example, if you invest £100, £0.50 goes to stamp duty and £99.50 is used to buy shares.

This happens on every buy order involving UK stocks, including auto-investments and rebalancing within a pie.

When investing in ETFs on Trading 212, you typically don’t pay stamp duty directly, even if the ETF holds UK-listed stocks. This is because ETFs are structured as funds, and any stamp duty incurred from buying underlying UK shares is handled at the fund level, not by individual investors. The cost is effectively wrapped into the ETF’s ongoing performance and reflected in its total return. S

o, while you’re not charged the 0.5% stamp duty upfront like with direct stock purchases, the impact of those costs is still indirectly passed on through slightly lower fund performance over time.

In terms of other taxes there are so many variables at play at the personal level its not possible for me to explain the intricacies of global investing taxes that it would make this vide about 4/5 times as long.

How did I build this portfolio?

People often like to deconstruct this portfolio or ask questions why something is added or not added.

So the first part of this section I would like to say that I am very happy for you to make custom changes or use it as a base for you to change around however you like.

I also don’t even mind you taking it as a base and then sharing it as a social pie if you have made what you consider to be improvements.

As long as you don’t say that yours is specifically endorsed by me take it as a creative commons or something where you can use it for your own purposes.

But I would like to explain the general premise behind the choices.

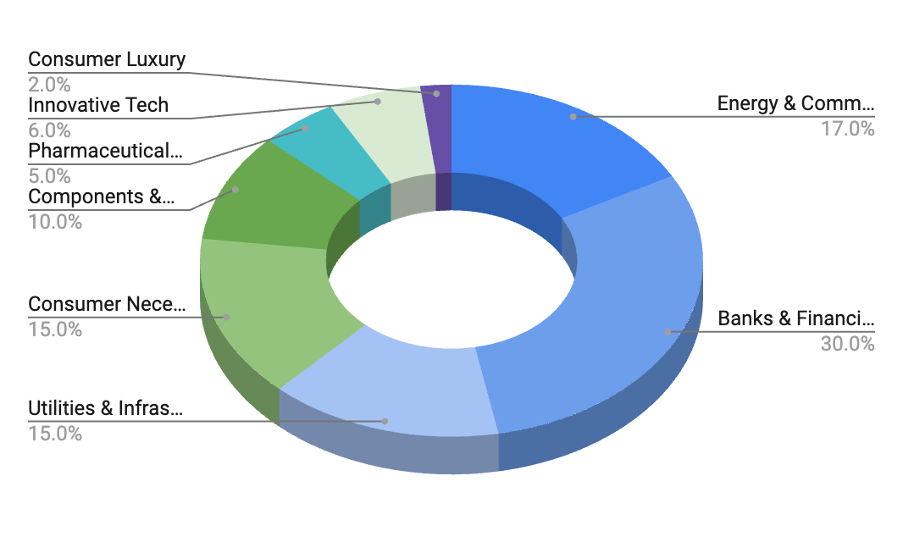

The Sector Divisions

Many dividend investors find the standard GICS sector system unhelpful because it groups together companies with very different business models and dividend profiles. For example, the Communication Services sector includes both AT&T, a steady dividend payer, and Netflix, which doesn’t pay dividends at all. To solve this, I created a more dividend-focused sector classification that highlights where natural dividend payers are most likely to be found — mature, profitable companies with predictable cash flows.

Categories like Utilities, Real Estate, and Banks tend to be strong sources of reliable dividends, while sectors like Innovative Tech or Consumer Luxury often aren’t.

I made a video explaining this in more detail here:

So, the categories I used are based on these which may seem unfamiliar if you haven’t seen this video before but not super critical to understand.

This is what the allocation looks like for reference at the time of making this video and you will be able to view this on the accompanying sheet too.

If you want to see the current yield and more details about the holdings you can view it here

So, I will give a general background that should give an idea of why that stock or that kind of stock is included within the pie.

And of course, any of the companies mentioned are subject to change.

Previous changes in the pie have been where stocks have been bought out or acquired which is quite prevalent in the UK market.

I will just go through the sectors and stocks now…

Energy and Commodities

In my view, energy and commodities can be a decent place to find natural dividend payers, but they come with a few caveats.

I’ve grouped them together because, realistically, energy has mostly been reduced to oil, gas, and coal, with all the infrastructure elements now sitting under utilities.

The sector is pretty cyclical, so while you can get solid dividends especially from the big supermajors like Shell or BP, you have to be prepared for some volatility. These companies tend to do well when commodity prices are high, but during downturns, dividends can get cut.

So, while I do include them in my dividend-focused categorisation, I’d stick to the larger, more established players if you’re looking for more reliable income as you will see from the choices below.

Rio Tinto (RIO.L)

I think Rio Tinto is a solid choice in the energy and commodities category for dividend investors because it’s a large, well-established mining company with strong cash flows and a consistent history of returning profits to shareholders.

The business focuses on essential raw materials like iron ore and copper, things the world always needs, which gives it a degree of resilience. While it’s still exposed to commodity price cycles, Rio tends to pay generous dividends, especially during boom periods, and often supplements its regular payout with special dividends when profits are strong.

Glencore plc (GLEN.L)

Glencore is a diversified commodities trader and miner, and while it operates in a cyclical sector, it has historically paid attractive dividends when commodity prices are strong. Its payouts can be inconsistent, but during profitable years, the company tends to return significant cash to shareholders, often including special dividends and buybacks.

Shell plc (SHEL.L)

Shell is a classic example of a supermajor energy company with a long history of paying dividends. While it cut its dividend during the 2020 oil crash, it has since rebuilt its payout and remains a staple for income investors looking for exposure to the energy sector with global diversification.

BP plc (BP.L)

BP, like Shell, is a large, integrated oil and gas company that offers solid dividends, especially appealing when energy markets are strong. Its dividend was also reset in 2020, but management has reaffirmed a commitment to shareholder returns through both payouts and share buybacks.

Utilities and Infrastructure

I consider Utilities & Infrastructure one of the best sectors for dividend investors. These companies are typically very stable because they operate under licenses or regulation that essentially guarantee their place in the market – they’d have to seriously mess up to lose that.

They’re often allowed a set level of profit, which gives them the ability to consistently return cash to shareholders. While they usually have high capital costs and aren’t the most explosive growers, they make up for it by being really reliable when it comes to paying dividends.

I would also include telecoms in this category, since in today’s world they’re pretty much core infrastructure too.

National Grid plc (NG.L)

National Grid is a dependable dividend payer, benefiting from its role as a regulated utility. Its revenues are relatively stable, and the company has a strong track record of consistent, inflation-linked dividend growth, making it a favourite for conservative income investors.

Greencoat UK Winds (UKW.L)

Greencoat UK Wind invests in operational wind farms and generates revenue through long-term power purchase agreements. It pays a regular dividend and is structured to deliver stable, predictable income which is highly attractive for dividend-focused investors in the renewables space.

SSE plc (SSE.L)

SSE is a UK energy company focused on electricity generation and transmission. It’s known for offering strong dividends, supported by regulated operations and renewables expansion. It’s seen as a reliable income stock, especially for those looking to invest in the clean energy transition.

Renewables Infrastructure Group (TRIG.L)

TRIG invests in renewable energy assets across the UK and Europe. It targets a stable and attractive dividend yield, funded by predictable cash flows from long-term contracts. Like UKW, it’s structured to be a steady income vehicle in the infrastructure space.

United Utilities Group plc (UU.L)

United Utilities is a regulated water company, which makes its earnings and dividend payments highly predictable. It has a long-standing policy of growing its dividend in line with inflation, making it a solid choice for risk-averse income investors.

BT Group plc (BT-A.L)

BT has historically paid dividends, but its payout has been volatile in recent years due to restructuring, pension obligations, and capital investment needs. Since that it shows promising of returning to itself “old self”. While it may return to consistent dividends, it’s more speculative compared to traditional utility peers.

Components and Production

I think Components & Production is a solid sector for dividend investors, though maybe not quite as stable as Utilities.

I created this category to capture companies that are more manufacturing or hardware-focused like traditional industrials, but also including things like medical device makers or hardware-based tech firms.

These businesses often produce tangible goods that are in consistent demand, and many of them reach a mature stage where they generate steady profits and return a decent chunk to shareholders.

It’s not the highest-yielding category across the board, but there are definitely some reliable dividend payers here, especially among the more established players.

BAE System plc (BA.L)

BAE Systems is a leading defence contractor with a strong and reliable dividend record. Its revenues are largely backed by long-term government contracts, which makes cash flow stable and predictable. It has a long history of growing dividends steadily and is well-regarded among income investors.

Coca-Cola HBC AG (CCH.L)

Coca-Cola HBC is a bottling partner for Coca-Cola products across several markets. It offers decent dividend yields, supported by consistent earnings and strong cash generation. While not a massively high-yielder, it’s relatively stable and benefits from a defensive, consumer-oriented business model.

Bunzl plc (BNZL.L)

Bunzl is a distribution and outsourcing company serving a wide range of industries. It has a long track record of dividend growth, supported by steady revenue and a defensive business model. It’s not a high-yield stock but is considered reliable for dividend compounding.

Banks and Financials

Banks & Financials is another strong sector for dividend investors in my view. These companies deal directly with capital – moving it, managing it, and profiting from it – so it makes sense that they often return a portion of that capital to shareholders.

Banks, insurance firms, asset managers, and even business development companies generally have the kind of steady cash flow needed to support dividends.

That said, they can get hit during economic downturns, and sometimes regulators step in to pause or limit payouts, like we saw during the pandemic.

But overall, they tend to bounce back quickly and resume dividends, making this sector a reliable source of income for long-term investors.

Barclays plc (BARC.L)

Barclays offers a variable but generally attractive dividend. As a major UK bank, its payouts depend heavily on the economic cycle and regulatory environment. Dividends were suspended during the pandemic but have since resumed. It’s more volatile than some financial peers but can offer solid income in stronger markets.

HSBC Holdings plc (HSBA.L)

HSBC is one of the most globally diversified banks and historically has been a reliable dividend payer. Although it paused dividends during the COVID-19 crisis due to regulatory restrictions, it has reinstated them and remains a cornerstone in many dividend-focused portfolios.

NatWest Group plc (NWG.L)

NatWest has returned to paying dividends after years of restructuring post-financial crisis. It currently offers an attractive yield, but given its history and sensitivity to UK economic conditions, it’s more suitable for income investors comfortable with some risk.

Legal & General Group plc (LGEN.L)

Legal & General is a strong dividend stock in the insurance and asset management space. It has a dependable yield and a history of consistent growth, backed by robust cash flows and a conservative capital structure. It’s a favourite among long-term dividend investors.

M&G (MNG.L)

M&G, an asset manager spun out from Prudential, has offered a very high yield since listing, aiming to attract income investors. While the yield is appealing, sustainability has occasionally come into question, so we will be worth monitoring payout ratios and earnings closely.

Aviva plc (AV.L)

Aviva has cleaned up its business in recent years and refocused on its core markets, which has strengthened its ability to pay dividends. It currently offers a strong yield and is aiming to return more cash to shareholders, including through buybacks.

Lloyds Banking Group plc (LLOY.L)

Lloyds pays a solid dividend with room for growth, supported by its retail banking dominance in the UK. It’s sensitive to economic conditions and interest rates, but remains a staple for many dividend portfolios seeking exposure to UK financials.

Phoenix Group Holdings plc (PHNX.L)

Phoenix is a specialist in life insurance and closed-book business, and it offers one of the highest dividend yields in the FTSE 100. Its cash flow is stable due to its predictable business model, making it very attractive to income-focused investors.

Aberdeen Group plc (ABDN.L)

Aberdeen Group pays a decent dividend, but its business performance has been mixed in recent years. As an asset manager, it’s sensitive to market conditions and fund flows. While the yield is attractive, we still need to watch for signs of sustained recovery.

Consumer Necessity

Consumer Necessity is one of the better sectors for dividend investing. These are companies that sell products people keep buying regardless of economic conditions. These are things like food, household goods, tobacco, and alcohol.

In economic terms, they have low price elasticity of demand, meaning people don’t cut back much even if prices rise or their income falls. So, necessity in that sense rather than a true-life necessity – as tobacco is clearly not.

That kind of consistent demand usually leads to steady revenues and profits, which in turn supports reliable dividends. Some of these companies might not have the highest yields, but they often have long track records of uninterrupted or even growing payouts, which is exactly what I look for in a natural dividend payer.

Unilever plc (ULVR.L)

Unilever is a classic dividend stock with a strong track record of consistent payouts and modest dividend growth. Its global portfolio of essential consumer goods supports stable earnings, making it a go-to defensive choice for long-term income investors.

Associated British Foods plc (ABF.L)

ABF owns a mix of businesses including Primark and food brands. It has a more modest dividend compared to peers but is financially strong and tends to pay conservatively. Its payout is stable, though not high, making it suitable for balancing out portfolios.

Tesco plc (TSCO.L)

Tesco pays a moderate dividend supported by its strong position in UK retail. After a few rocky years and a dividend suspension, it’s now back to regular payouts. The yield is competitive, and the business model is defensive enough for income investors.

Tate & Lyle plc (TATE.L)

Tate & Lyle, focused on food ingredients, pays a reliable dividend supported by a steady, low-cyclicality business. It’s not a high-yielder but has a good history of maintaining payouts and benefits from exposure to long-term food trends.

A.G. BARR plc (BAG.L)

A.G. BARR, maker of soft drinks like IRN-BRU, offers a modest but reliable dividend. It has a clean balance sheet and a disciplined approach to shareholder returns, making it a stable if unspectacular option for dividend seekers.

British American Tobacco plc (BATS.L)

BATS is one of the highest-yielding dividend stocks in the FTSE 100. Its cash flows are very strong, supported by addictive products and global scale. I have never had a stock more requested than Britihs American Tobacco in the previous version of the pie but can understand if you would prefer to exclude it

Imperial Brands plc (IMB.L)

Imperial Brands also offers a very high dividend yield, backed by consistent earnings from tobacco products. The company has recently refocused on core markets and cost control, helping to stabilise its payout after some prior concerns.

Pharmaceuticals and Medical Research

Pharmaceuticals & Medical Research isn’t my go-to sector for dividend investing, at least not in most cases.

A lot of companies in this space, especially early-stage biotechs, are still in heavy R&D mode and really shouldn’t be paying dividends. They need to reinvest in drug development, and if they’re successful, the return on that investment is likely far greater than any dividend would be.

That said, once a pharmaceutical company reaches a certain size, think big pharma like the choices in this pie — it can start to behave more like a Consumer Necessity business, supplying essential, widely used medicines. At that stage, they can become reasonable dividend payers, but early on, I’d rather let them focus on growth and revisit them later if they mature into natural dividend payers.

AstraZeneca plc (AZN.L)

AstraZeneca pays a modest dividend, but the focus is on reinvestment and R&D rather than high income. It’s a strong company with solid growth prospects, but not ideal if dividend yield is your primary goal.

GSK plc (GSK.L)

GSK has historically paid a generous dividend, but recent restructuring and spin-offs (e.g., Haleon) have affected its consistency somewhat. It remains a decent payer but is in a transition phase, so that’s something to be aware of.

Innovative tech

Innovative Tech is probably one of the worst sectors for dividend investing, at least from my perspective.

These companies are usually focused on rapid growth, product development, and scaling, which means they’re reinvesting profits (or often running at a loss) rather than paying anything out to shareholders.

That’s not a bad thing for growth investors, but it doesn’t really work for a dividend-focused strategy.

Even when some of these companies become profitable, they tend to use that cash for buybacks or further expansion. If they ever do reach a mature stage, they often shift into other categories like Consumer Luxury or Components & Production. Until then, I’d generally avoid Innovative Tech when building an income portfolio. As you will see from the stocks lumped into this sector they are not strictly innovative tech, in the case of this pie you could think of this more like a miscellaneous sector than innovative tech as such.

MONY Group plc (MONY.L)

MONY Group plc, trading as Money Supermarket, is a British company which specialises in technology-led money-saving platforms including several price comparison websites. It operates in the financial comparison sector and is not yet a core income stock. Yield is moderate and still developing post-spinout.

The Sage Group plc (SGE.L)

Sage is a software company that provides steady, growing dividends, though the yield is relatively low. It’s attractive for long-term income investors looking for tech exposure with some cash return rather than rapid growth.

WPP plc (WPP.L)

WPP, a global advertising and marketing firm, pays a respectable dividend, though it has been somewhat inconsistent during downturns. The company has returned to a more stable payout policy recently and offers modest yield with growth potential.

Consumer Luxury

Consumer Luxury isn’t a great sector for dividend investing in my opinion. These companies sell non-essential, often high-end products, things people cut back on when the economy gets tough.

That means their revenues and profits can be pretty sensitive to economic cycles, and as a result, their dividends tend to be less reliable. You might see a high yield from time to time, especially from companies like automakers or fashion brands, but those payouts can disappear quickly if sales drop.

The inconsistency makes it hard to count on them for long-term income, so I usually steer clear of this category when building a dividend-focused portfolio. The choice in this sector has been surprisingly resilient even during downturns so it’s a rare addition in this sector added to the pie.

Games Workshop Group plc (GAW.L)

Games Workshop is a niche but highly profitable company that has paid out generous and sometimes special dividends, supported by strong margins and loyal customer base. While not a traditional dividend stock, it has become a favourite among growth-minded income investors.

How to Learn More about this Sort of Thing?

Since the last FAQ and the (literally 1000s) of questions I have had, I’ve been working on something special – a project that’s honestly taken way too long to get just right.

For those looking to improve their investing knowledge, I’m thrilled to finally share it with you: The Dividend Academy!

The Dividend Academy is a platform for anyone who wants to grow their wealth through smart investing.

Whether you’re new to investing or looking to add some new strategies, this course is all about building wealth and having a better understanding of what exactly you are doing in the stock market.

At The Dividend Academy, the focus is on actionable knowledge. This isn’t just about theory—you’ll be equipped to make informed investing decisions.

Easy-to-Follow Lessons:

The course is structured in a way that’s easy to follow. Lessons are delivered through engaging, animated videos that break down even the most complex topics, making them simple to understand. Even if you’ve never invested before, you’ll be able to pick up new strategies quickly and confidently.

Diverse Investment Strategies:

Despite the name – dividend investing is not the only strategy covered. You’ll learn about a variety of approaches to building wealth, allowing you to tailor your investment journey to fit your own goals and lifestyle.

Constant Updates:

Markets and trends are always shifting, so the course keeps evolving, too. You’ll receive lifetime future access to every update, keeping you in the loop on the latest techniques, no matter how much the investing landscape changes.

Supportive Community

By joining The Dividend Academy You also get premium lifetime membership to the premium tier of the Dividend Temple Discord too. That comes as an added bonus of your enrolment fee

Investing can sometimes feel like a solo journey, but it doesn’t have to. As a member, you’ll join The Dividend Temple, a community of investors where you can ask questions, share tips, and get insights from others on the same path.

It’s a supportive, judgment-free zone to learn and grow.

One of the biggest advantages of The Dividend Academy is lifetime access. You pay once, and that’s it.

No additional costs for future updates, no subscription fees—just a lifetime of access to every piece of content that is added over time.

You can check that all out on TheDividendAcademy.com

Conclusion

I hope that this guide has helped you decide whether or not the UK income Factory pie is for you.

Even if you watched all this video and got to this point and you took in all this information and now decided that the UK Income Factory pie is not for you, I would still consider that a huge success in terms of explaining the pie.

Something that people don’t seem to realise is that I don’t actually get anything when people copy the pie. It actually doesn’t make a material difference to me at all if 1 person copies or 1 million people copy, therefore I never try to get people to invest in it and would much prefer you find something that suits your own goals.

If that is the UK Income factory portfolio, then welcome aboard!

If that’s not the UK Income factory portfolio, then I appreciate you taking the time to read everything on this page and would love to see you as a Subscriber on the Youtube Channel and maybe see something you do find interesting on there!